.avif)

Cost Control vs Cost Management: Understanding the Key Differences

TL;DR

Pelanor is reimagining cloud cost management with AI-native FinOps tools that explain spending, not just track it. By rebuilding the data layer from scratch, we deliver true unit economics across complex multi-tenant environments - revealing what each customer, product, or team actually costs. Our AI vision is deeper: we're building systems that truly reason about infrastructure, learning what's normal for your environment and understanding why costs change, not just when.

Every business leader faces the same fundamental challenge: managing finances effectively while driving growth. Yet many organizations struggle because they confuse two critical concepts—cost control and cost management. While these terms might sound interchangeable, understanding their distinct roles can mean the difference between merely surviving and strategically thriving.

Cost control focuses on immediate expense management and budget compliance, while cost management takes a strategic, long-term approach to optimizing your entire cost structure. Both are essential, but they serve different purposes in your financial strategy. This guide will help you understand when to apply each approach, how to implement them effectively, and most importantly, how to leverage both for maximum business impact.

What is Cost Control?

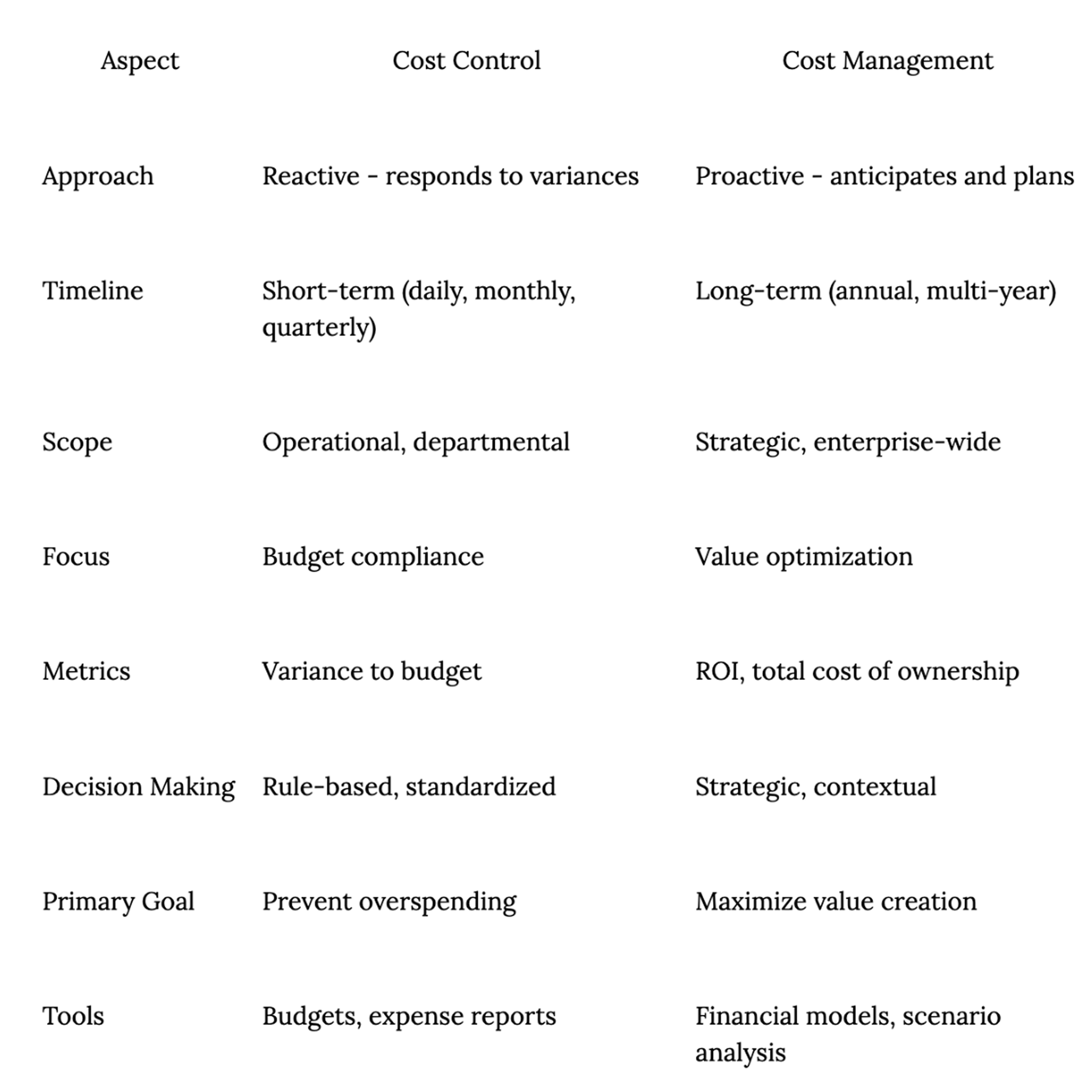

Cost control is the systematic process of monitoring and regulating expenses to ensure they stay within predetermined budgets. It's fundamentally a reactive approach—you set spending limits, track actual expenses against those limits, and take corrective action when costs threaten to exceed boundaries.

At its core, cost control focuses on the here and now. It asks questions like: Are we overspending? Where can we cut back? How do we bring expenses back in line? This approach emphasizes containment rather than optimization, making it particularly valuable when immediate financial discipline is needed.

The primary objectives of cost control include maintaining budget compliance, preventing cost overruns, ensuring operational efficiency, and providing real-time visibility into spending patterns. It's about maintaining financial stability through disciplined expense management.

Core Principles of Cost Control

The foundation of effective cost control rests on several key principles. Budget adherence forms the cornerstone—every expense must align with predetermined allocations. This isn't just about having budgets; it's about treating them as firm commitments rather than loose guidelines.

Variance analysis plays a crucial role in cost control. By regularly comparing actual expenses to budgeted amounts, organizations can quickly identify problem areas. When marketing spend jumps 20% above budget in Q2, cost control mechanisms trigger immediate investigation and correction. This continuous monitoring ensures small problems don't become major financial crises.

Expense monitoring provides the real-time data that makes cost control possible. Modern organizations track spending daily, sometimes hourly, using sophisticated financial systems. This granular visibility enables rapid response when costs begin drifting off course.

Corrective actions complete the cost control cycle. When variances occur, predetermined protocols kick in—perhaps requiring additional approvals for over-budget expenses or implementing temporary spending freezes in specific departments. These actions aren't punitive but protective, ensuring resources remain available for critical business needs.

Common Cost Control Techniques

Organizations employ various techniques to maintain cost control. Budget caps establish hard limits on spending categories, preventing departments from exceeding allocated resources without executive approval. These caps might be monthly, quarterly, or project-based, depending on organizational needs.

Approval hierarchies create checkpoints for spending decisions. Purchases above certain thresholds require multiple sign-offs, ensuring oversight increases with expense magnitude. A $500 office supply order might need manager approval, while a $50,000 software purchase requires C-suite involvement.

Expense tracking systems provide the technological backbone for cost control. From enterprise resource planning (ERP) platforms to specialized spend management tools like Pelanor's platform, these systems capture, categorize, and report on every dollar spent. Modern solutions increasingly leverage AI to identify patterns and anomalies that human reviewers might miss.

Regular financial reporting keeps stakeholders informed about cost performance. Weekly department reports, monthly variance analyses, and quarterly reviews create accountability and transparency around spending patterns. These reports don't just track numbers—they tell stories about organizational behavior and identify opportunities for improvement.

What is Cost Management?

Cost management represents a fundamentally different philosophy—it's a proactive, strategic approach that views costs not just as expenses to control, but as investments to optimize. Rather than simply asking "How do we spend less?", cost management asks "How do we spend smarter?"

This comprehensive approach encompasses the entire cost lifecycle, from initial planning through execution and analysis. Cost management integrates financial decisions with business strategy, recognizing that today's cost structure shapes tomorrow's competitive position.

Where cost control reacts to variances, cost management anticipates and plans for them. It considers not just the immediate price tag but the total cost of ownership, opportunity costs, and strategic value of every financial decision. This forward-thinking approach transforms cost from a constraint into a strategic enabler.

Strategic Elements of Cost Management

Strategic planning forms the foundation of cost management. Organizations develop multi-year cost strategies aligned with business objectives, considering how cost structures should evolve to support growth, innovation, and market positioning. This isn't about creating rigid long-term budgets but about understanding how costs should transform as the business evolves.

Forecasting extends beyond simple budget projections to include scenario planning and sensitivity analysis. Cost managers model various business conditions, preparing strategies for different economic environments, competitive landscapes, and growth trajectories. What happens to our cost structure if revenue grows 50%? What if a competitor enters with disruptive pricing? These questions drive strategic thinking.

Optimization strategies seek to maximize value from every dollar spent. This might involve renegotiating vendor contracts for better terms, investing in automation to reduce long-term labor costs, or redesigning processes to eliminate waste. The goal isn't always spending less—sometimes it's spending more in areas that generate disproportionate returns.

Long-term financial planning ensures cost decisions support sustainable growth. Rather than cutting training budgets to meet quarterly targets, cost management might increase training investment to build capabilities that reduce future operational costs. This patient approach requires discipline but delivers compound benefits over time.

Cost Management Methodologies

Activity-based costing (ABC) allocates costs based on actual resource consumption rather than arbitrary percentages. This methodology reveals the true cost of products, services, and processes, enabling more informed strategic decisions. At Pelanor, we've seen how AI-enhanced analytics can supercharge ABC implementation, automatically identifying cost drivers that traditional analysis might overlook.

Value engineering systematically analyzes functions to identify opportunities for cost reduction without sacrificing quality or performance. Teams examine each component and process, asking whether there's a more cost-effective way to deliver the same value. Sometimes a minor design change can eliminate significant costs without affecting customer experience.

Lifecycle costing considers total costs from acquisition through disposal. A cheaper piece of equipment might have higher maintenance costs and shorter lifespan, making it more expensive over time than a pricier alternative. This comprehensive view prevents false economies that plague short-term thinking.

Strategic cost analysis examines cost structures in the context of competitive positioning and market dynamics. Organizations analyze their cost position relative to competitors, identifying areas where cost leadership or differentiation strategies make sense. Not every business needs the lowest costs—sometimes premium cost structures support premium positioning.

Key Differences Between Cost Control and Cost Management

Understanding the distinctions between cost control and cost management helps organizations apply each approach appropriately. While both aim to optimize financial performance, they differ fundamentally in philosophy, scope, and execution.

The most significant difference lies in their temporal orientation. Cost control focuses on present expenses, managing what's happening now. Cost management looks forward, shaping future cost structures. Cost control asks "Are we over budget this month?" while cost management asks "Will our cost structure support our five-year strategy?"

Their scope also varies dramatically. Cost control typically operates at the departmental or project level, managing discrete budget line items. Cost management takes an enterprise-wide view, considering how costs in one area affect performance elsewhere.

Reactive vs Proactive Approaches

Cost control's reactive nature means it responds to problems after they emerge. When travel expenses spike, cost control implements new approval requirements or reduces travel budgets. This approach works well for maintaining discipline but may miss opportunities for strategic improvement.

Cost management's proactive stance identifies issues before they become problems. By analyzing travel patterns, a cost management approach might negotiate corporate rates with preferred vendors, implement virtual meeting technology, or redesign processes to reduce travel needs while maintaining business effectiveness.

Consider a manufacturing company facing rising material costs. Cost control might respond by cutting other expenses to stay within budget. Cost management would analyze the entire supply chain, potentially identifying alternative materials, negotiating long-term contracts, or investing in equipment that uses materials more efficiently.

Scope and Timeline Differences

Cost control operates in the immediate term, typically focusing on current month or quarter performance. Its scope is necessarily limited—addressing specific variances in particular departments or projects. This narrow focus enables quick action but may overlook systemic issues.

Cost management embraces longer horizons and broader perspectives. It considers how today's decisions affect next year's cost structure and how investments in one area might generate savings elsewhere. This comprehensive view reveals opportunities invisible to pure cost control approaches.

Strategic Integration

Cost control typically operates independently of strategic planning, focusing on operational efficiency within existing structures. It accepts current business models and processes as given, seeking to execute them more efficiently.

Cost management integrates deeply with strategic planning, recognizing that cost structures should evolve with business strategy. When organizations enter new markets, launch products, or transform operations, cost management ensures financial structures support these initiatives.

Benefits of Cost Control

Despite its reactive nature, cost control delivers significant value, particularly in maintaining financial discipline and operational efficiency. Organizations need these benefits to ensure short-term stability while pursuing longer-term strategic objectives.

Immediate Financial Impact

Cost control's greatest strength lies in its ability to deliver quick financial wins. When organizations face cash flow challenges or profit pressures, cost control measures can improve financial performance within weeks or months.

Budget adherence prevents the financial surprises that can derail business plans. By maintaining spending within predetermined limits, organizations ensure they have resources available for critical investments and unexpected opportunities. This predictability enables better planning and reduces financial stress.

The discipline imposed by cost control creates a culture of financial responsibility. When employees understand that budgets matter and overspending has consequences, they make more thoughtful spending decisions. This cultural shift often delivers benefits beyond pure cost savings.

Operational Efficiency Gains

Cost control drives operational efficiency by forcing organizations to scrutinize every expense. This examination often reveals waste, redundancy, and inefficiency that might otherwise go unnoticed. What starts as cost pressure becomes operational improvement.

Process improvements frequently emerge from cost control initiatives. When forced to reduce expenses, teams often discover better ways of working that deliver equal or better results with fewer resources. These innovations might never surface without cost pressure as catalyst.

Benefits of Cost Management

While cost control maintains stability, cost management drives transformation. Its strategic approach creates sustainable competitive advantages that compound over time.

Long-term Strategic Value

Cost management aligns financial structures with business strategy, ensuring organizations have the cost flexibility to compete effectively. This alignment becomes particularly valuable during industry disruptions or economic shifts when agility determines survival.

Competitive advantages emerge when organizations optimize their cost structures more effectively than rivals. Lower cost positions enable aggressive pricing strategies, while efficient operations free resources for innovation and growth investments.

Innovation and Optimization Opportunities

Cost management's analytical approach reveals opportunities for innovation that pure cost control might discourage. By understanding true cost drivers, organizations can redesign products, services, and processes for dramatically better economics.

Investment in technology and automation often emerges from cost management analysis. While requiring upfront capital, these investments can transform cost structures, turning fixed costs into variable ones or eliminating cost categories entirely.

When to Use Cost Control vs Cost Management

Choosing between cost control and cost management isn't an either-or decision—it's about applying the right approach to the right situation. Understanding when each method works best helps organizations maximize their effectiveness.

Cost Control Scenarios

Crisis situations demand cost control's immediate impact. When organizations face cash crunches, profit warnings, or economic downturns, cost control provides the rapid response needed to stabilize finances.

Budget overruns trigger cost control mechanisms. When departments consistently exceed allocations or projects spiral beyond planned costs, cost control reestablishes discipline and accountability.

Operational inefficiencies often require cost control's focused attention. When specific processes or departments show excessive costs relative to benchmarks or historical performance, targeted cost control can restore efficiency.

Cost Management Applications

Strategic planning phases require cost management's comprehensive approach. When developing long-term strategies, entering new markets, or considering major investments, cost management ensures financial structures support strategic objectives.

Growth initiatives benefit from cost management's forward-looking perspective. Scaling businesses need cost structures that can grow efficiently, maintaining or improving unit economics as volume increases.

Transformation programs demand cost management's systemic view. Whether digitizing operations, restructuring organizations, or redesigning business models, cost management ensures new structures deliver intended benefits.

Implementation Strategies

Building a Cost Control System

Start by establishing clear budgets with realistic targets based on historical performance and business requirements. Ensure every department and project has defined spending limits with understood consequences for overruns.

Implement robust tracking mechanisms that capture expenses in real-time or near-real-time. Modern expense management platforms can automatically categorize spending, flag variances, and generate alerts when predetermined thresholds are approached. The integration capabilities of platforms like Pelanor ensure that data flows seamlessly from multiple sources, providing a comprehensive view without manual data entry.

Create approval workflows that balance control with operational flexibility. Develop reporting cadences that keep stakeholders informed without overwhelming them. Establish governance structures with clear roles and responsibilities.

Developing a Cost Management Framework

Begin with strategic alignment, ensuring cost management objectives support broader business goals. Build analytical capabilities to understand true cost drivers and relationships. This might require investing in costing systems, analytical tools, and skilled personnel who can model complex cost scenarios.

Create planning processes that integrate cost management with strategic planning. Develop optimization methodologies tailored to your industry and business model. Implement performance metrics that balance short-term control with long-term value creation.

Common Challenges and Solutions

Cost Control Challenges

Resistance to budget constraints often emerges when cost control feels arbitrary or punitive. Address this by involving operational leaders in budget setting, explaining the rationale behind limits, and celebrating teams that achieve objectives within budget.

Over-restriction can stifle growth and innovation when cost control becomes too rigid. Balance this by maintaining separate innovation budgets, allowing flexibility for strategic investments, and regularly reviewing whether cost control measures still serve business objectives.

Cost Management Implementation Hurdles

Complexity can overwhelm organizations attempting comprehensive cost management. Simplify by beginning with pilot programs in specific areas, focusing on the most significant cost drivers first, and gradually expanding scope as capabilities mature.

Cultural change represents perhaps the biggest challenge, as cost management requires shifting from reactive to proactive thinking. Drive change by securing leadership commitment, celebrating early wins to build momentum, and embedding cost management thinking in planning processes.

Integrating Cost Control and Cost Management

The most effective organizations don't choose between cost control and cost management—they integrate both approaches into comprehensive financial management strategies. This integration leverages each approach's strengths while mitigating their individual weaknesses.

Cost control provides the foundation of financial discipline and operational efficiency. Cost management builds on this foundation, optimizing structures for competitive advantage and sustainable growth. Together, they create a robust financial management system that addresses both immediate needs and long-term objectives.

Technology increasingly enables integration by providing platforms that support both immediate control and strategic analysis. Solutions like Pelanor's comprehensive platform bridge the gap between tactical cost control and strategic cost management through unified data and intelligent analytics.

How Pelanor Can Help?

At Pelanor, we understand that effective financial management requires both disciplined cost control and strategic cost management. Our AI-powered solutions automate routine cost control tasks while providing the analytical insights needed for strategic cost management.

Our platform integrates seamlessly with your existing financial systems through extensive integration capabilities, ensuring complete visibility into your cost structure without disrupting current operations. We work with you to implement the right balance of cost control and cost management, ensuring your financial strategy supports rather than constrains your business objectives.

Frequently Asked Questions

Is cost control better than cost management?

Neither approach is inherently superior—their effectiveness depends entirely on your organizational context and objectives. Cost control excels at maintaining financial discipline and delivering quick wins, making it essential during crises or when operational efficiency is paramount. Cost management creates sustainable competitive advantages through strategic optimization, proving invaluable for growth and transformation initiatives. Most successful organizations employ both approaches, using cost control for immediate oversight while leveraging cost management for strategic advantage.

What are the main tools for cost control?

Effective cost control relies on several key tools working in concert. Budgeting software establishes and tracks spending limits across departments and projects. Expense tracking systems capture and categorize every transaction, providing real-time visibility into spending patterns. Variance analysis tools compare actual expenses to budgets, flagging deviations that require attention. Approval workflow platforms ensure appropriate oversight for spending decisions. Reporting dashboards keep stakeholders informed about cost performance.

Can small businesses benefit from cost management?

Absolutely—cost management principles apply regardless of organization size, though implementation approaches should scale appropriately. Small businesses might start with simple cost management techniques like analyzing customer profitability, optimizing vendor relationships, or identifying their true cost drivers. As they grow, they can adopt more sophisticated methodologies. The key advantage for small businesses is their agility—they can often implement cost management insights faster than larger competitors.

What industries rely most heavily on cost control?

Manufacturing industries traditionally emphasize cost control due to thin margins and intense competition. Retail businesses rely on cost control to maintain profitability despite price pressure and changing consumer preferences. Healthcare organizations use cost control to manage expenses while maintaining quality standards and regulatory compliance. Airlines and hospitality businesses, with their high fixed costs and volatile demand, depend on cost control for financial stability.

How do you measure cost management success?

Cost management success requires multifaceted measurement beyond simple expense reduction. Return on investment (ROI) for cost initiatives indicates whether improvements deliver expected value. Unit economics trends show whether cost structures improve as businesses scale. Total cost of ownership metrics reveal the true long-term impact of decisions. Competitive cost positioning indicates whether your cost structure provides market advantages.

What's the difference between cost reduction and cost control?

Cost reduction actively decreases expenses through specific initiatives—eliminating positions, renegotiating contracts, or discontinuing services. It's an action-oriented approach focused on lowering absolute spending levels. Cost control maintains expenses within predetermined limits without necessarily reducing them. It's about discipline and oversight rather than active cutting.